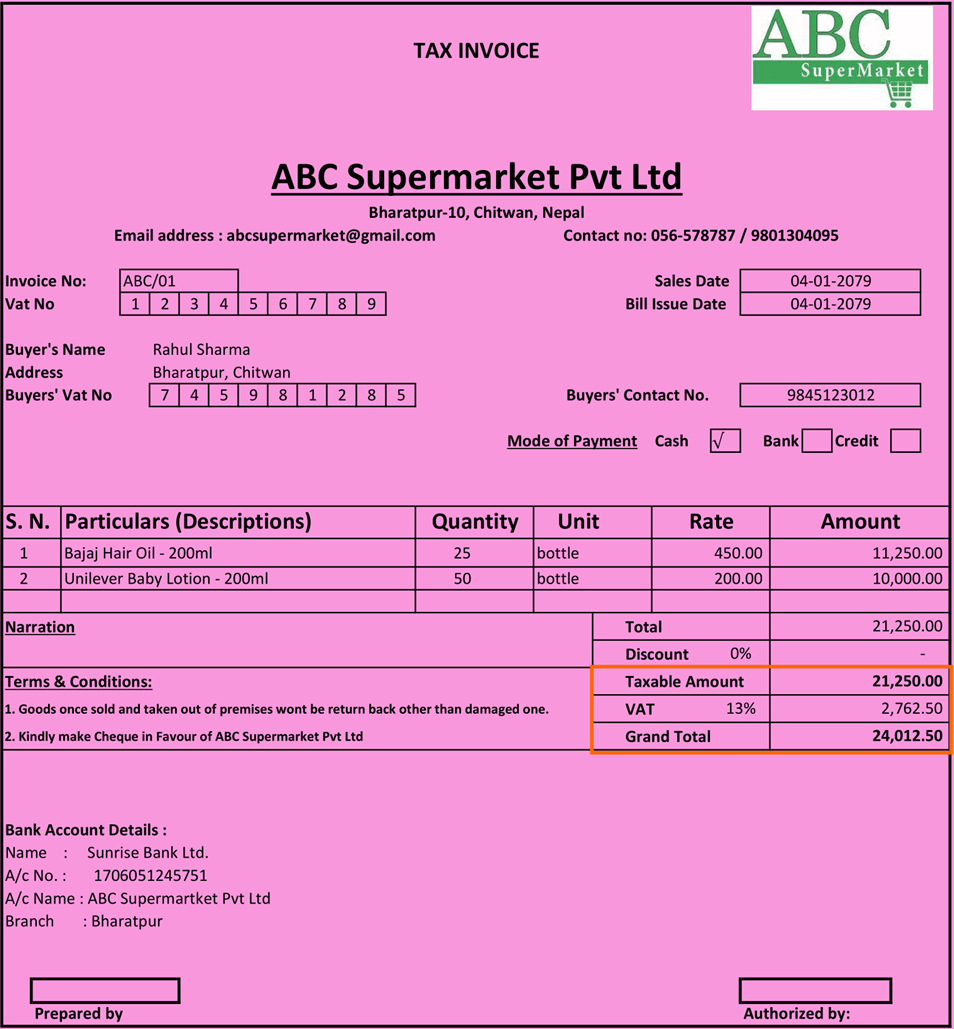

VAT is applicable on point of sales which means it is charged on the sales price of goods and services. It is required to be shown as an addition to the sales price in the invoice provided to the customer shown below:

Following are the compliance requirement relating to invoices applicable to VAT-registered entities:

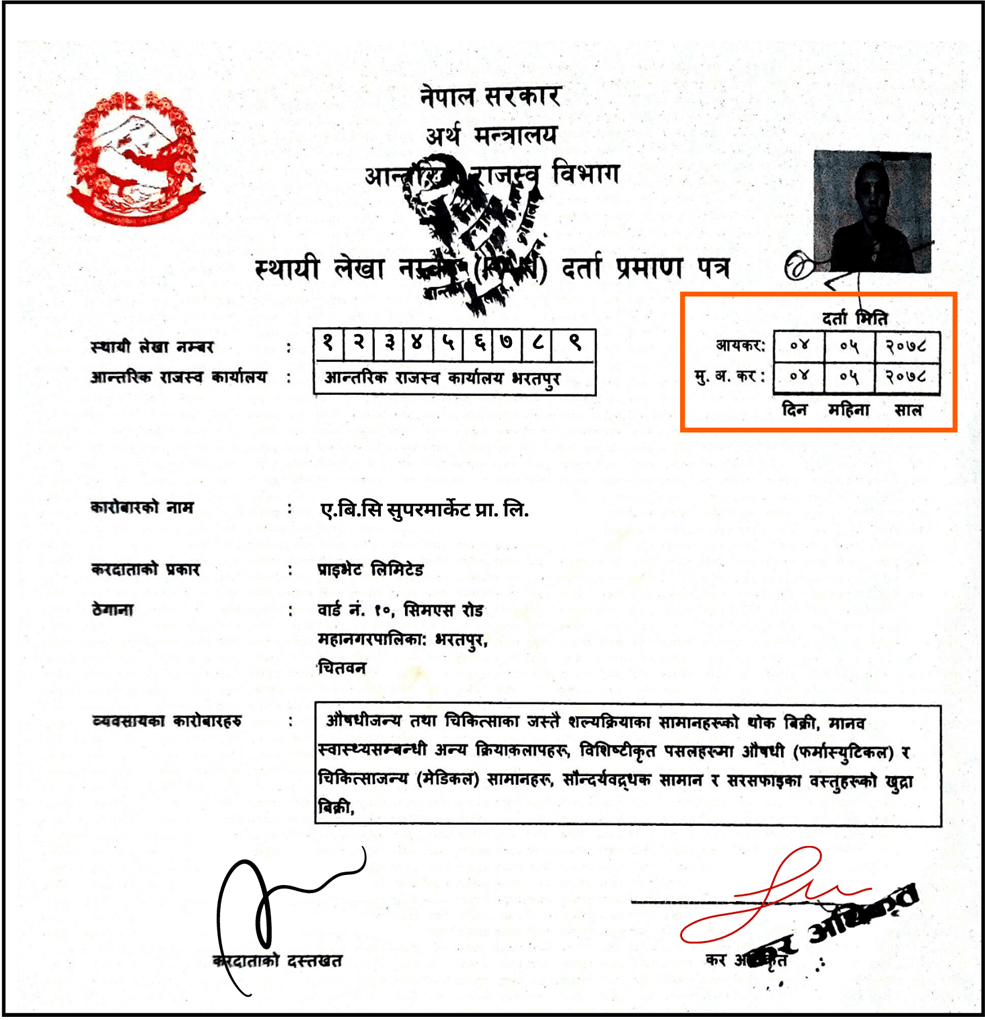

- VAT No of the seller should be mentioned.

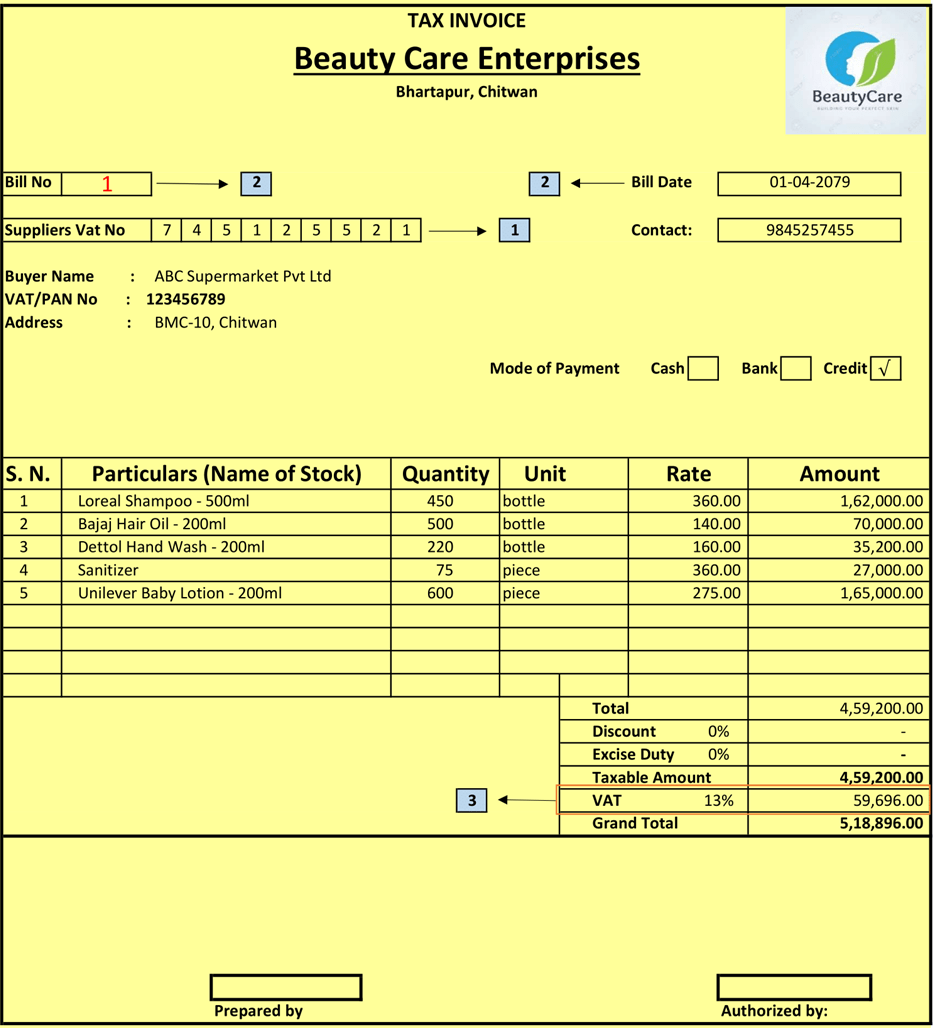

- The invoice should be drawn in chronological order starting from 01

(Remember no invoice no can be left blank, and invoices cannot be drawn on expired or future dates)

- The invoice should be drawn in chronological order starting from 01

- VAT Rate and Amount should be mentioned in the invoice.

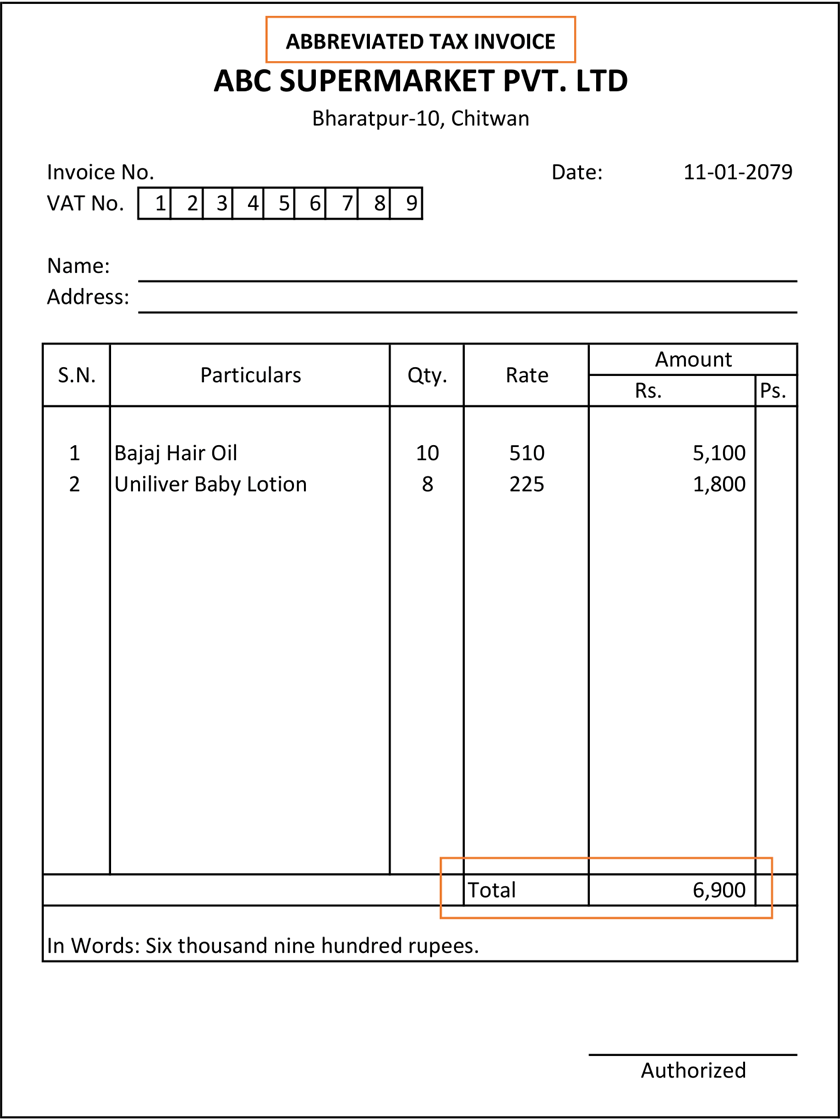

Abbreviated Invoice:

For a business entity that deals with a high inflow of retail customers and needs to display the final price, inclusive of VAT to attract customers, it might not be practical to draw a VAT Invoice for every sale made. Restaurants, Grocery stores or supermarkets, etc are some examples of such entities. These business entities can seek approval from the revenue department to use abbreviated invoices. In such invoices, the VAT amount is not shown separately and the price of goods and services sold is inclusive of VAT. However, upon request by the customer, they need to issue a proper VAT Invoice.

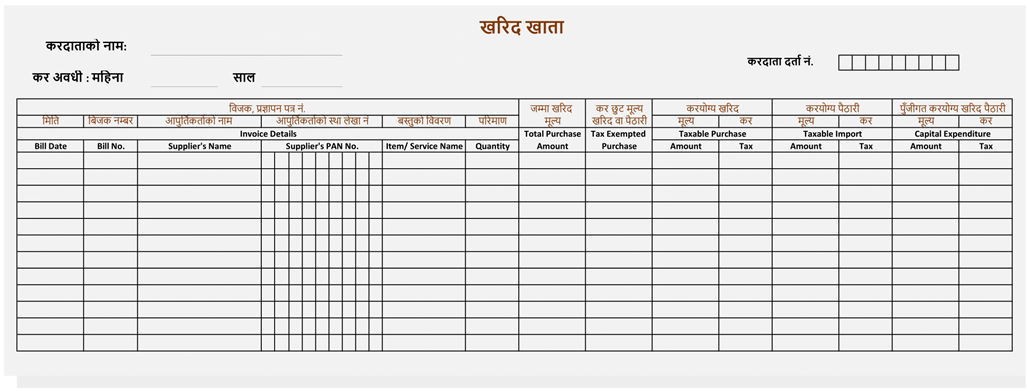

This book maintains a detailed record of each purchase made in a month. The purchase should be classified as either stock, fixed asset, import, or purchase of VAT exempted items. Any purchase return should also be recorded as a negative amount. The amount of total purchase and VAT total, as per this book is entered as Total Purchase and VAT on Purchase in VAT Return.

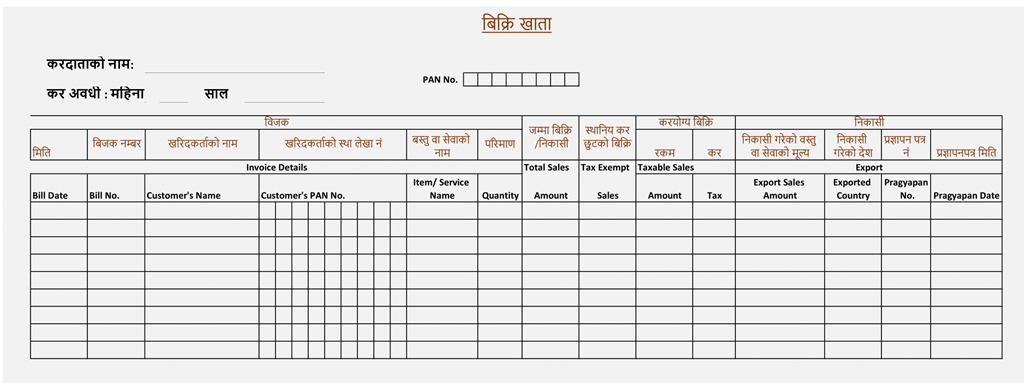

This book maintains a detailed record of each sale made in a month. Sales should be classified as domestic sales, export, or sale of VAT exempted items. Businesses must record details of Sales returns & canceled Invoices. The total sales and VAT total, as per this book, are entered as Total Sales and VAT on Sales in VAT Return.

Business Entities who draw invoices electronically using software approved by IRD are not required to maintain Physical books of Kharid Khata and Bikri Khata if their software can generate reports of sales and purchases in the format just as physical Kharid Khata and Bikri Khata.

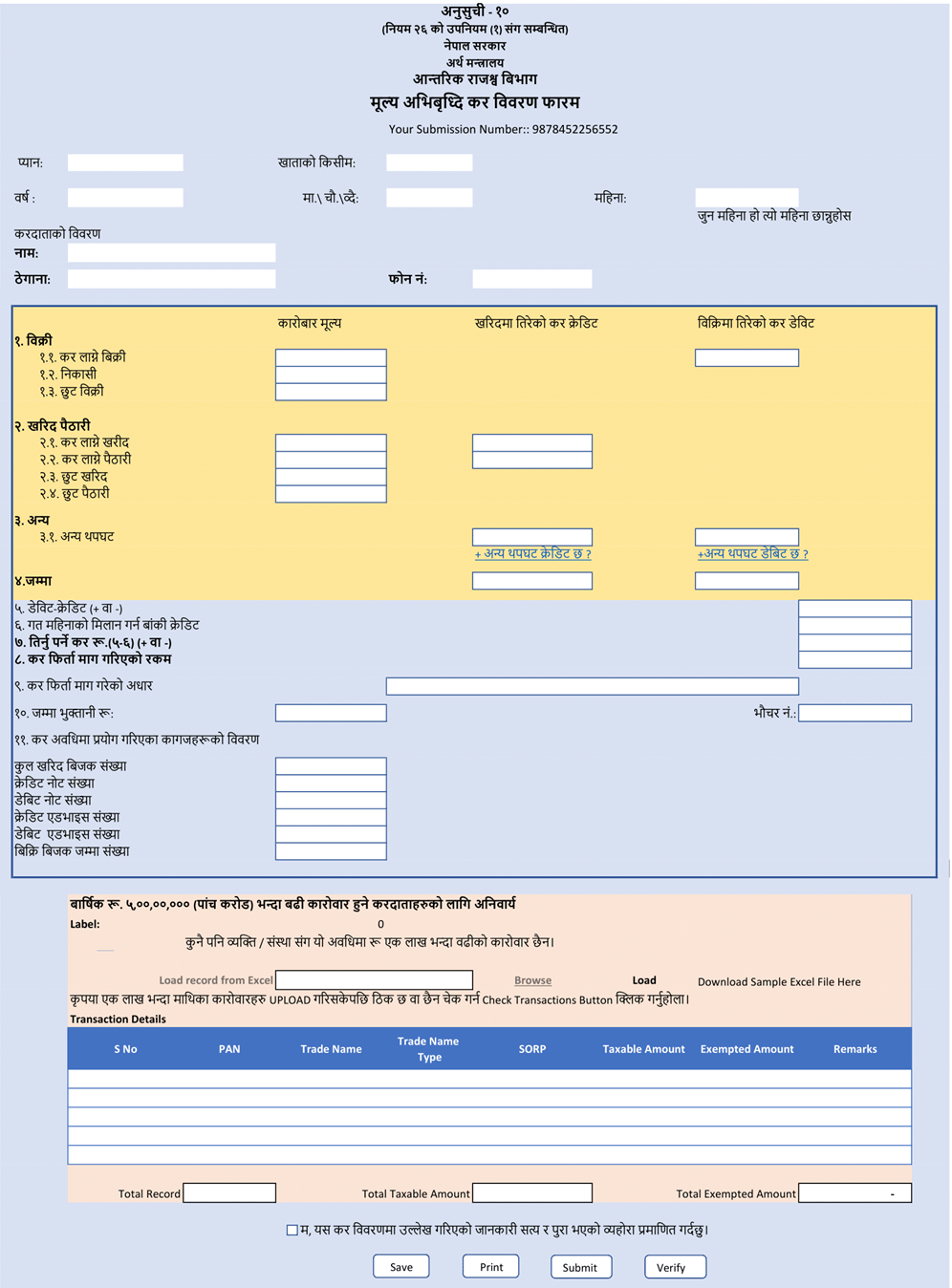

VAT Return is basically an online form used to calculate VAT Liability for any month. We have to fill in details about:

- Net Sales amount and VAT Output

- Net Purchase amount and VAT Input

- VAT Adjustment

- VAT Credit Amount carried forward from the previous period

- Transaction details of sales and purchase exceed 1 lakh if the total turnover of the business cross 5 crores in the current or previous fiscal year.

There is no separate area to mention Purchase Return or Sales Return. These have to be adjusted with the gross purchase or sales amount. Sales Amount shall be the total sales as recorded in Bikri Khata. Similarly, Purchase Amount shall be the total purchase as recorded in Kharid Khata.