NFRS 1: First-time Adoption of International Financial Reporting Standards

NFRS 1 provides guidelines for companies adopting it for the first time. It provides criteria, structure and framework necessary for conversion for GAAP to NFRS.

NFRS 2: Share-Based Payment

NFRS 2 makes companies include share-based payments (like shares, options, or rights) in their financial statements. It covers transactions settled in cash or company shares, with specific guidelines for each.

NFRS 3: Business Combinations

NFRS 3 outlines how to account for business combinations (like mergers or acquisitions) using the ‘acquisition method.’ It measures assets and liabilities at fair values on the acquisition date. The main benefit is that it allows easy comparison of different companies because they present data on the same basis.

NFRS 4: Insurance Contracts

NFRS 4 applies to all insurance contracts issued by a company, including reinsurance contracts.

NFRS 5: Non-current Assets Held for Sale and Discontinued Operations

NFRS 5 guides how to account for assets that a company plans to sell or distribute to owners. These assets are not depreciated, measured at the lower of carrying amount or fair value minus selling costs, and shown separately in the financial statements. Specific disclosures are required for discontinued operations and asset disposals.

NFRS 6: Exploration for and Evaluation of Mineral Resources

NFRS 6 lets companies keep using their old accounting policies for exploration and evaluation assets when they adopt the standard for the first time. It also changes how companies test for impairment of these assets by introducing new indicators and allowing testing at a combined level.

NFRS 7: Financial Instruments: Disclosures

NFRS 7 requires companies to disclose the importance of financial instruments and the risks they pose. They must provide both qualitative and quantitative information. Specific details are needed for transferred financial assets and other related matters.

NFRS 8: Operating Segments

NFRS 8 requires certain companies to disclose information about their business segments, products, services, geographic areas, and major customers. They use internal management reports to identify and measure this information.

NFRS 9: Financial Instruments

NFRS 9 tells us how to recognize and measure financial instruments, deal with impairment, recognition, and general hedge accounting.

NFRS 10: Consolidated Financial Statements

NFRS 10 guides how to prepare consolidated financial statements. Companies must consolidate entities they control, meaning they have power to influence profits and affect returns.

NFRS 11: Joint Arrangements

NFRS 11 explains accounting for arrangements jointly controlled by multiple companies. Joint control means sharing control. The arrangements are classified as joint ventures (sharing net assets) or joint operations (having rights and obligations).

NFRS 12: Disclosure of Interests in Other Entities

NFRS 12 requires companies to share details about their interests in subsidiaries, joint arrangements, associates, and unconsolidated ‘structured entities’.

NFRS 15: Revenue from Contract

The most important standard; NFRS 15 explains how and when a company following NFRS will record revenue and requires them to give more useful information in their financial statements. The rule uses a simple five-step model that applies to all contracts with customers.

NFRS 16: Lease Accounting

NFRS 16 explains how companies using NFRS should handle leases. It requires lessees to recognize assets and liabilities for most leases, while lessors continue classifying leases as operating or finance.

NAS 1: Presentation of Financial Statements

NAS 1 provides rules for organizing financial statements, including their structure, guidelines, and the necessary information they must contain. It requires presenting a full set of financial statements every year and including the amounts from the previous year.

NAS 7: Cash Flow Statement

NAS 7 explains how to show data in a cash flow statement. It tells us about the company’s cash and cash equivalents and how they are changed bifurcating them into operational, investment and financial categories.

NAS 8: The Accounting Policies, Changes in Accounting Estimates and Errors

NAS 8 provides guidelines for selecting and changing accounting policies, handling changes in accounting estimates, disclosing policy changes, and correcting errors.

NAS 10: Events after the Reporting Period

NAS 10 tells companies when they should adjust their financial statements for events that occur after the reporting period. It also guides companies on disclosing information about when the financial statements were authorized for issue and events that happened after the reporting period.

NAS 12: Income Taxes

NAS 12 guides how companies should handle income taxes based on taxable profits. It requires recognizing deferred tax liabilities or assets for temporary differences, with a few exceptions.

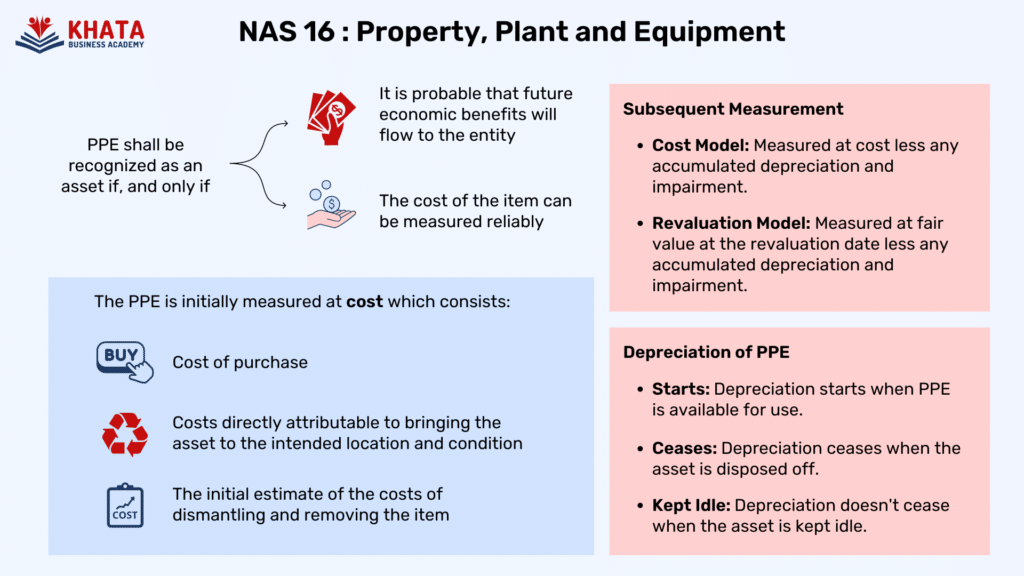

NAS 16: Property, Plant, and Equipment

NAS 16 sets rules for companies to recognize property, plant, and equipment as assets. It also explains how to measure their carrying amounts, calculate depreciation charges, and handle impairment losses.